The ICE Manufacturing Pivot

Making gas-powered vehicles is a hard business. Making a shift to electric will be even harder.

Manufacturing vehicles based on the internal combustion engine (ICE) has been one of the world’s best businesses for more than a half century, but it didn’t start that way. I enjoyed this whole article from 1930 (republished by the Saturday Evening Post) but this quote was on point:

From my pocket I took a clipping from the New York World of November 17, 1895, and asked him to read it. He brushed it aside. I insisted. It was an interview with Thomas A. Edison: “Talking of horseless carriage suggests to my mind that the horse is doomed. The bicycle, which, 10 years ago, was a curiosity, is now a necessity. It is found everywhere. Ten years from now you will be able to buy a horseless vehicle for what you would pay today for a wagon and a pair of horses. The money spent in the keep of the horses will be saved and the danger to life will be much reduced.”

Certainly that’s not a sentiment that inspires a future where the wealthiest countries in the world would design their entire transportation infrastructure around the technology one day. The necessities of world wars and the excellence of manufacturing brought to bear by Ford and later improved upon by Toyota, cemented ICE vehicles as the standard and economies all of the world experienced prosperity unlike the world had seen previously. Throughout the 20th century there were some experiments with electric vehicles (EVs) but it wasn’t until the1990s a new challenger entered the domain, the GM EV1. From the Department of Energy’s History of the Electric Car:

Fast forward again -- this time to the 1990s. In the 20 years since the long gas lines of the 1970s, interest in electric vehicles had mostly died down. But new federal and state regulations begin to change things. The passage of the 1990 Clean Air Act Amendment and the 1992 Energy Policy Act -- plus new transportation emissions regulations issued by the California Air Resources Board -- helped create a renewed interest in electric vehicles in the U.S.

During this time, automakers began modifying some of their popular vehicle models into electric vehicles. This meant that electric vehicles now achieved speeds and performance much closer to gasoline-powered vehicles, and many of them had a range of 60 miles.

One of the most well-known electric cars during this time was GM’s EV1, a car that was heavily featured in the 2006 documentary Who Killed the Electric Car? Instead of modifying an existing vehicle, GM designed and developed the EV1 from the ground up. With a range of 80 miles and the ability to accelerate from 0 to 50 miles per hour in just seven seconds, the EV1 quickly gained a cult following. But because of high production costs, the EV1 was never commercially viable, and GM discontinued it in 2001.

22 years later, those high production costs are still with GM and the other titans of the ICE vehicle. Meanwhile, Tesla is building EVs faster and more profitably than ever. The pivot will not be easy and, if it is possible, the resulting companies will be unrecognizable.

The ICE Manufacturer’s Model

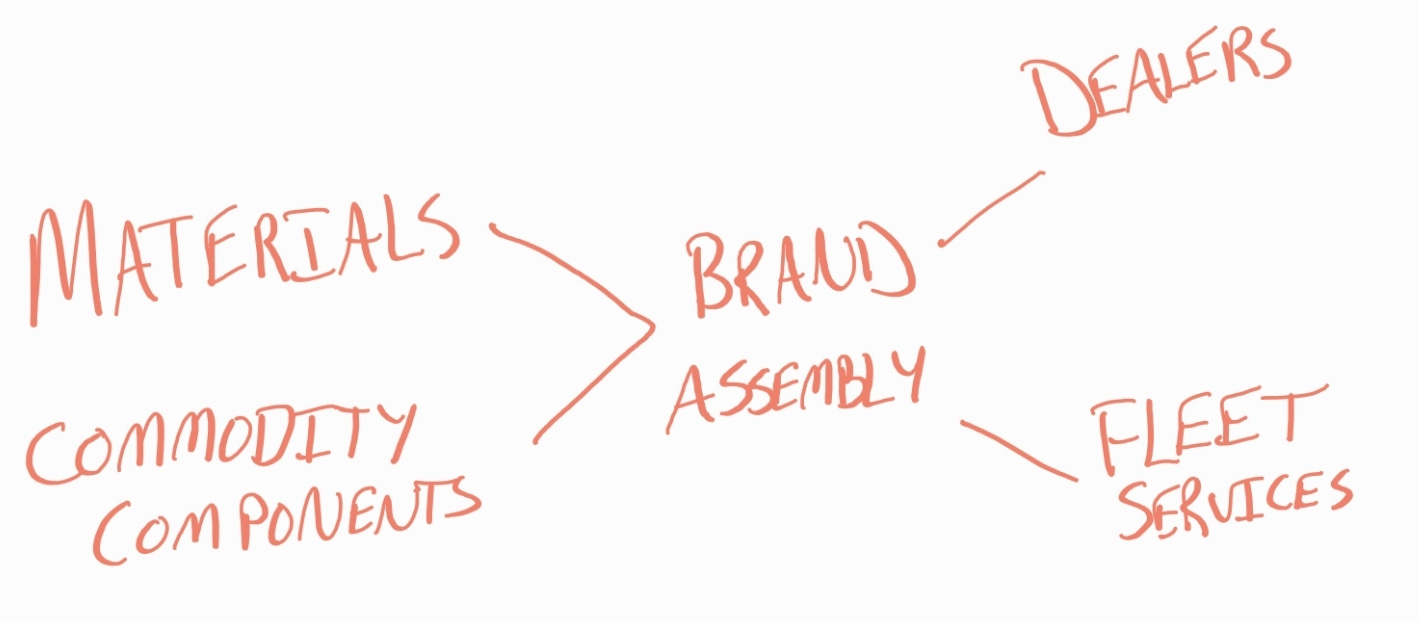

ICE vehicles are a marvel of technology. They combine an extremely complex system with a value add to consumer life that was unheard of prior to the dawn of the personal computer. That combination brought about two opportunities to innovate their business model and continue to grow long after the market was saturated.

The first innovation was planned obsolescence. This turned ICE vehicles from a functional transportation mechanism to a status symbol for all to see, while leveraging the manufacturing superiority already enjoyed by the dominant players. Refreshing the style of the vehicles year after year encouraged new purchases successfully, while leaving smaller operations to struggle to keep up and lose brand value with their stagnant models.

The second was dealership selling. CNN wrote up a nice history of how this came to be, but the key point of how it manifests today is ICE manufacturers are largely wholesalers, pushing the selling to the retailing dealerships and providing both vehicles and parts. Sales, delivery, and maintenance are labor intensive operations that are expensive to start up and scale, and ICE manufacturers today largely partner a huge number of local businesses with established relationships to their community.

These pillars hold up a business model that looks like this:

ICE Manufacturers are:

Selling vehicles

Selling aftermarket parts

Selling fleet management services

Selling the dream of the next vehicle

Then they are punting customer service for the consumer market to partners who have the relationship with the customers. This is a weak point and if 2 and 3 go away as a scalable business.

United Auto Workers See Cracks

From CTVC:

But the sudden gearshift to EVs is driving a wedge between autoworkers and automakers, coming down to profit, pay, and parts. Established automakers are playing defense against Tesla and other rising manufacturers, funneling billions of dollars in investments toward EV strategies while still trying to keep existing ICE business in the green. Ford’s EV business is expected to lose $4.5B this year even as the company plans to spend $50B on EVs through 2026.

"We need the ICE business to generate cash and the EV business to focus on innovation," CEO Jim Farley said in March. On Friday, Farley accused the UAW “holding the deal hostage over battery plants.”

Despite the promise of new plants and jobs, EVs require far fewer parts—like mufflers, catalytic converters, and fuel injectors—than their gasoline counterparts. An EV uses 40% less labor to assemble. This means fewer workers are needed to build and maintain EVs, and vehicle manufacturing jobs will quickly shift to battery ones. The UAW is worried about how this will affect their members.

This is a valid response by the UAW. They can see the market and government forces are putting pressure on Ford (and others) to move to EVs, but these publicly traded companies are struggling with keeping shareholders happy while they transition. The most natural place to squeeze is the labor force and that’s how the UAW came to be in the first place. Tesla (and by all accounts, Rivian and Lucid Motors) have no unionized labor force to contend with, so they continue pressing the advantage. These labor challenges can be expected to get worse over time for ICE manufacturers as their workers are asked to evolve their skillsets while accepting lower pay to keep the market happy in the face of pressure on margins. What’s unclear is if the UAW has enough clout to enter Tesla and level the playing field for the automakers at large.

Responses and Investments

Lobbying against EV incentives for decades was the road ICE manufacturers took as Tesla's rise brought the first real threat of an EV entrant. The Inflation Reduction Act shows that government investment in EVs isn't slowing down any time soon, so these businesses need a new response. Ford has mostly divested in Rivian at this point, and I think it is unlikely we see an acquisition or hedging investment strategy re-emerge. A direct pivot into EVs is going to be massively unprofitable for several years and would require either outside funding or keeping the competing ICE business alive to throw off the cash necessary for investment. Stock prices for these companies would be pummeled in the meantime while margins get squeezed. Nevermind the fact that the dealership model is not likely to survive the EV transition given the lack of maintenance revenue.

The major moves lately by Ford and GM have been to adopt the Tesla charging standard, thus punting charging network revenue to Tesla, and to double down on their subscription services and loyalty programs. This points to these companies pushing harder than ever into their fleet services and I do not think this will work. Businesses are rational buyers and why would I choose to pay for fleet services if the only real value is peace of mind and my own private charging station. The former is generally valuable to irrational consumers who are concerned with brand and the latter is largely an effort in one time paperwork.

So what is the best option? Disruption is hard to survive, but I think the move is to start building direct consumer relationships as fast as possible on the back of ICE vehicle sales. Dealerships are powerful but in urban settings, they are far less of a community pillar. I would start experimenting with new vehicle delivery direct from the factory and try to build a new consumer business focused on EVs in particular, while continuing wholesale of ICE vehicles to fleets. Ultimately though, there's a great amount of pain coming for ICE vehicle makers unless they can turn the tide of policy and public opinion back in their favor. I expect they’ll try to swim against the tide.