Duke Energy's quest for gas

Duke Energy's quest for gas

I imagine there's a lot of boardroom talk about gas/electricity synergies

Duke Energy has been in the news lately for updating its carbon plan for North Carolina to raise rates by up to 73% over the next 9 years and push out the 70% emissions reduction target (2005 baseline) set in North Carolina state law from 2030 to 2035. To better understand the context involved, I think it is useful to understand Duke’s business model and the great company context. Duke reports earnings just after I write this, so I plan to make a follow-up earnings analysis for Friday’s article.

A goal to grow

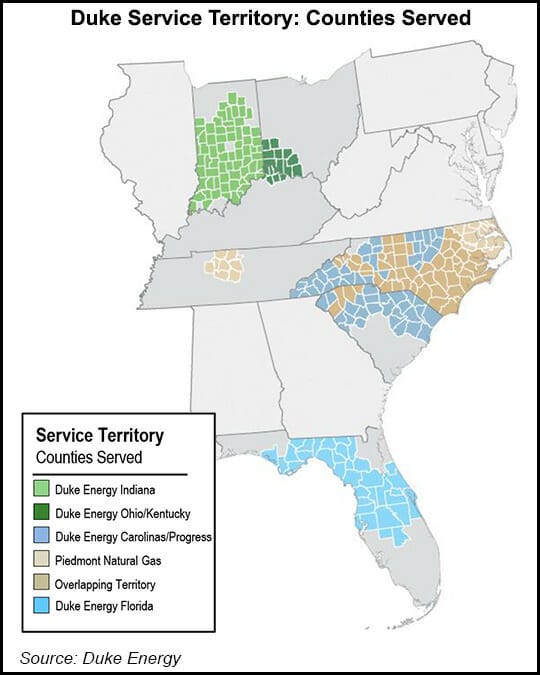

Duke has a mission to undertake large projects to limit regulatory overhead and generate low-risk returns for shareholders. This is a central reason why renewables present such an investment problem for vertically integrated utilities. Distributed energy resources are many small investments spread geographically and that is not how Duke does business. Duke has been careful to grow into markets where they can run as a vertically integrated utility, avoiding the deregulated regional transmission operator (RTO) markets for the most part. Their biggest presence is in Florida and North Carolina:

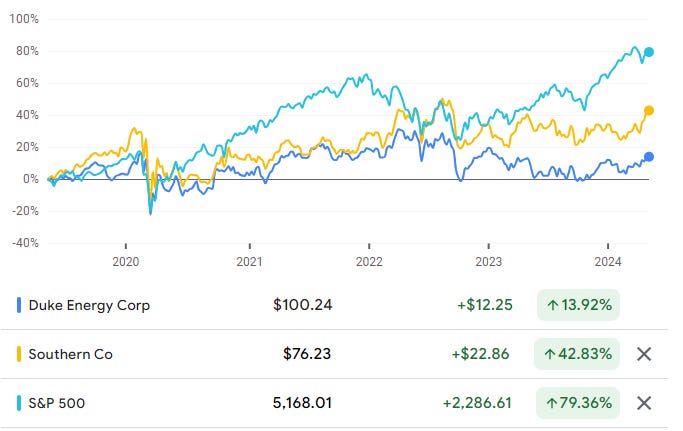

Throwing out NextEra Energy, which operates in every state with a much more diversified set of functions than any other utility company, Duke Energy competes with Southern Company for the largest electricity provider by market cap. This is largely thanks to each operating as vertically integrated utilities without competition (with a few exceptions). Shareholders love certainty with consistent returns as long as there is growth at some level. Growth can come from acquisitions but ideally, there would be new electricity demand that can help justify new power plants to be funded by ratepayers. Southern Company has had this tailwind for a few years with a manufacturing boom in its territory, Duke is hoping for a similar return to growth after years of lagging behind.

Gas begets gas

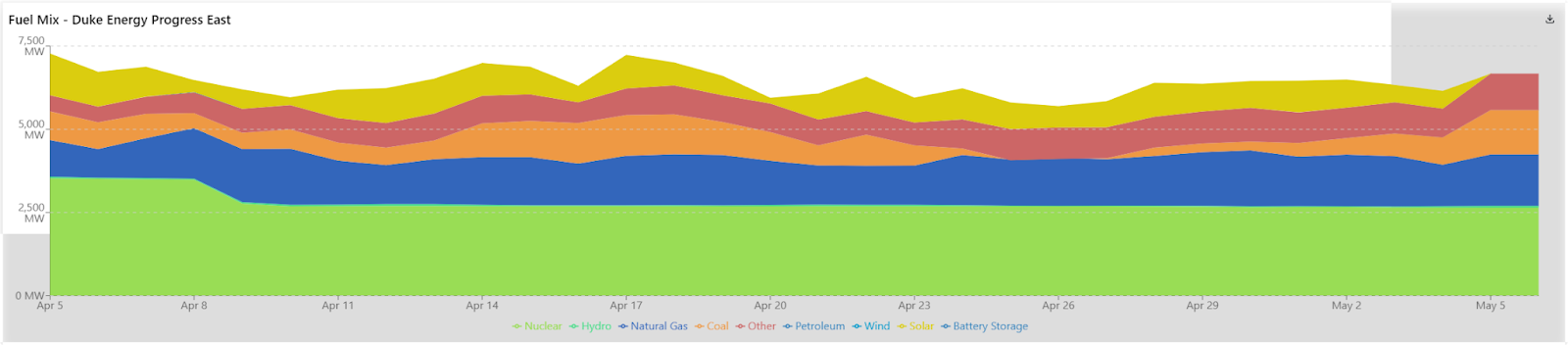

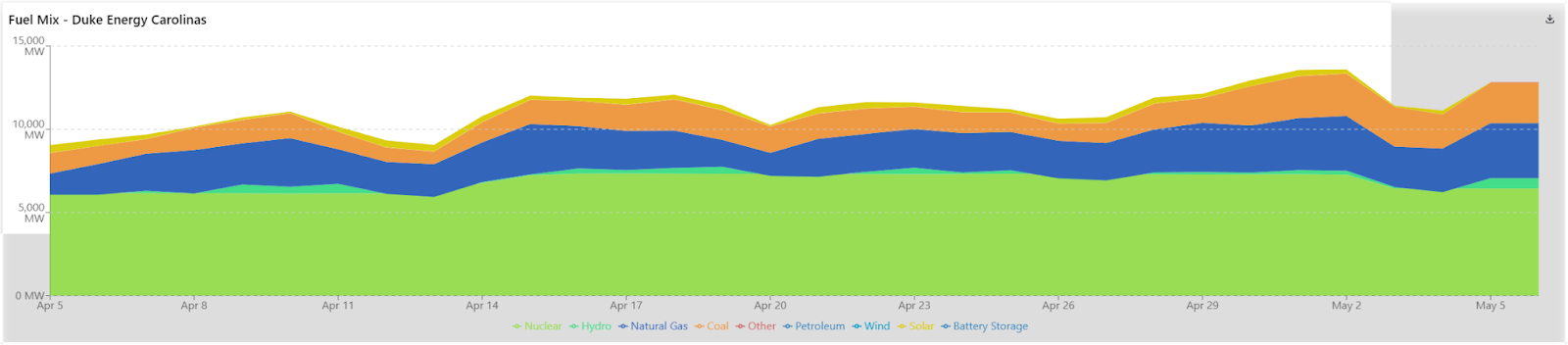

Around 15% of Duke’s business is in gas utilities and infrastructure. Geographically, the gas service area is mostly located within North Carolina, with a few pockets in Tennessee and South Carolina. From GridStatus we can get an idea of how this relationship with gas has affected the fuel mix in North Carolina over the years. Note that Duke has split North Carolina into two pieces due to some acquisition history, Duke Energy Progress is east and Carolinas is west.

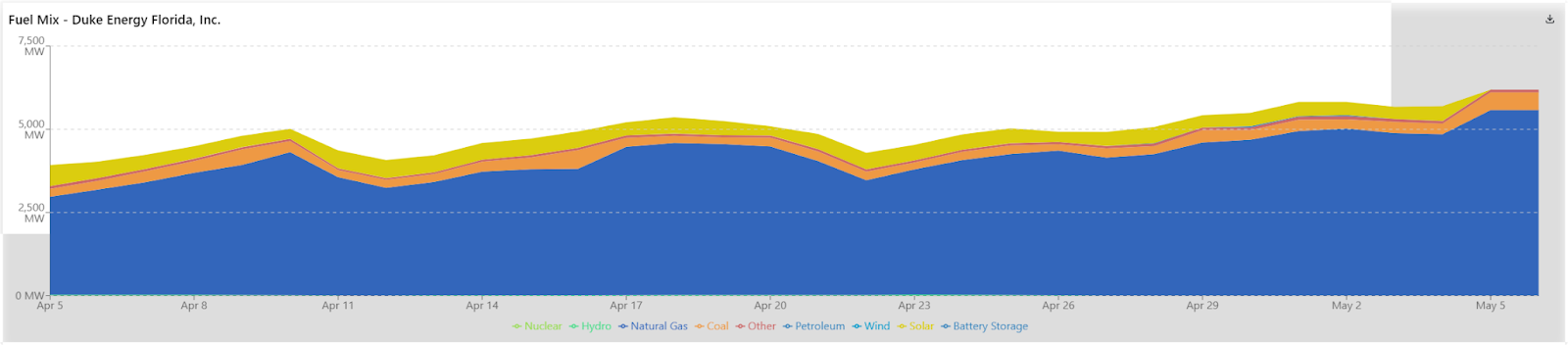

Florida utilities are adding solar at a rate faster than any other state. However, Duke Energy Florida again makes a play to expand gas infrastructure substantially in their forward-looking plan, matching solar additions with gas for a 50/50 mix going forward:

This plan includes a net addition of over 4,700 MW of solar PV generation with an expected equivalent summer firm capacity contribution of approximately 880 MW, 90 MW of firm storage added in 2027 and 430 MW of combustion turbine firm capacity added in years 2032 and 2033. The incorporation of the full firm capacity of the Osprey Energy Center takes place at the end of 2025. Between 2022 and 2027, DEF will add close to 400 MW of combined cycle capacity that results from projects focusing on increasing the fuel efficiency of the combined cycle generating units. DEF continues to consider market supply-side resource alternatives to enhance DEF’s resource plan.

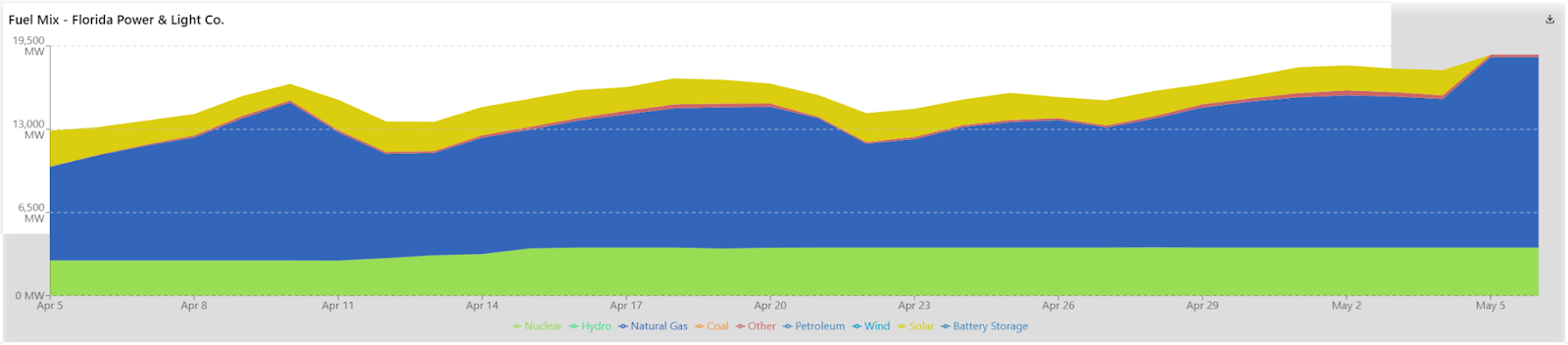

Even more interesting about Duke’s presence in the Sunshine State is that they don’t own the gas utility. That is owned by Chesapeake Utility Corporation operating as Florida Public Utilities. However, the ample presence of gas and the attraction of big capital expenditures to build more gas sweetens the deal. More gas may benefit Duke entering the gas market in Florida as well. Take a look at the other big utility in the area, Florida Light and Power (FLP), which runs two sizeable nuclear power stations:

There is a huge presence of gas for both thanks to FLP being owned by NextEra Energy, another combined utility serving both gas and electricity to customers.

Electricity from gas dynamics

Utilities that own both gas and electricity distribution are problematic for making good, market-driven choices on how electricity should be generated. There are some markets like PJM where gas dominates today, but the resource mix is much more diverse than we see in Florida. Duke Energy is looking to follow the same playbook in North Carolina by adding no more utility-scale solar than they add gas, allowing them to raise rates and return more money to shareholders. This is a poor choice for sunny, warm weather states because the dominant energy needs are for cooling, which aligns well with solar production hours. While industrial use cases may require more 24-hour power, the great presence of nuclear in North Carolina provides ample opportunity to generate as a firm resource at night, allowing a completely different dynamic.

I come back to this thought often: electricity markets are not free markets. As such, regulators need to understand the incentives for Duke Energy to use more gas going forward. If opening up the market to competition is not possible, the next best solution for ratepayers is to ensure the monopoly does not generate outsized profits for two of its businesses at once.